Personal Finance Basics in India 2026 (Free Tool)

Managing personal finance in India during 2026 has become a true life skill, much like driving through busy city traffic. It’s no longer something people can put off or ignore. With the fast-paced economy and rising costs, personal finance basics in India 2026 involve more than just handling numbers. They encompass habits, emotional decisions, family pressures, and choices made under stress or uncertainty. People earning from ₹20,000 to ₹2,00,000 a month often face confusion because money management touches different aspects of daily life.

Personal financial literacy builds a resilient system that protects against uncertainty, unexpected expenses, and lifestyle inflation.

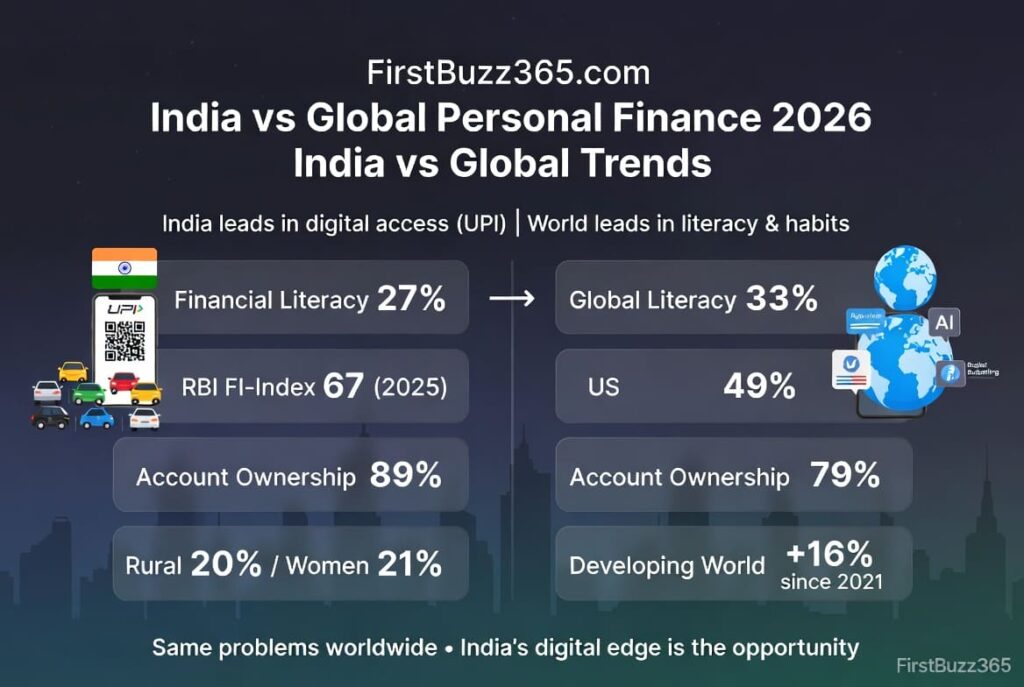

Financial literacy in India remains a pressing concern, with only 27% of adults considered financially literate according to the S&P Global FinLit Survey 2023—the latest comprehensive data available as of early 2026—marking a slight rise from 24% in 2019 but still lagging the global average of 33%.

The RBI’s Financial Inclusion Index reached 67 in March 2025, reflecting gains in access and usage, yet rural literacy stands at just 20% and women’s at 21% per the National Centre for Financial Education (NCFE) 2023 survey. This gap matters because financially literate individuals save 35% more and are 50% less likely to fall into debt traps, as noted in World Bank reports from 2023.

In the digital era, improving financial structure starts with leveraging apps for budgeting, online courses on platforms such as RBI’s financial literacy portal, and tools like UPI for automated transfers—turning overwhelming concepts into daily habits. Mastering credit discipline, emergency savings, tax efficiency, prudent investing, and retirement planning becomes essential. FirstBuzz365’s team is focused on providing real fundamentals—the elements that many overlook, misunderstand, or discover too late. Lets try to see personal finance in simple terms, like common pitfalls, and straightforward steps to bring clarity and control.

What Personal Finance Actually Means (Not the Fancy Definition)

Personal finance boils down to how individuals earn, spend, save, borrow, protect, and grow money over a lifetime. That’s the essence. It doesn’t revolve around stock tips, crypto hype, becoming rich overnight, or copying someone else’s strategy. Instead, good personal finance leads to calm rather than flashiness. It creates a system where money supports life goals without constant worry.

The key components include income from salary, freelance, business profit, or rental; expenses divided into fixed like rent and EMIs, and variable like food and entertainment; debt such as home loans, education loans, or credit cards; savings for emergency funds and short-term goals; investments for long-term wealth building; and protection through health and life insurance. Getting these in balance forms the foundation.

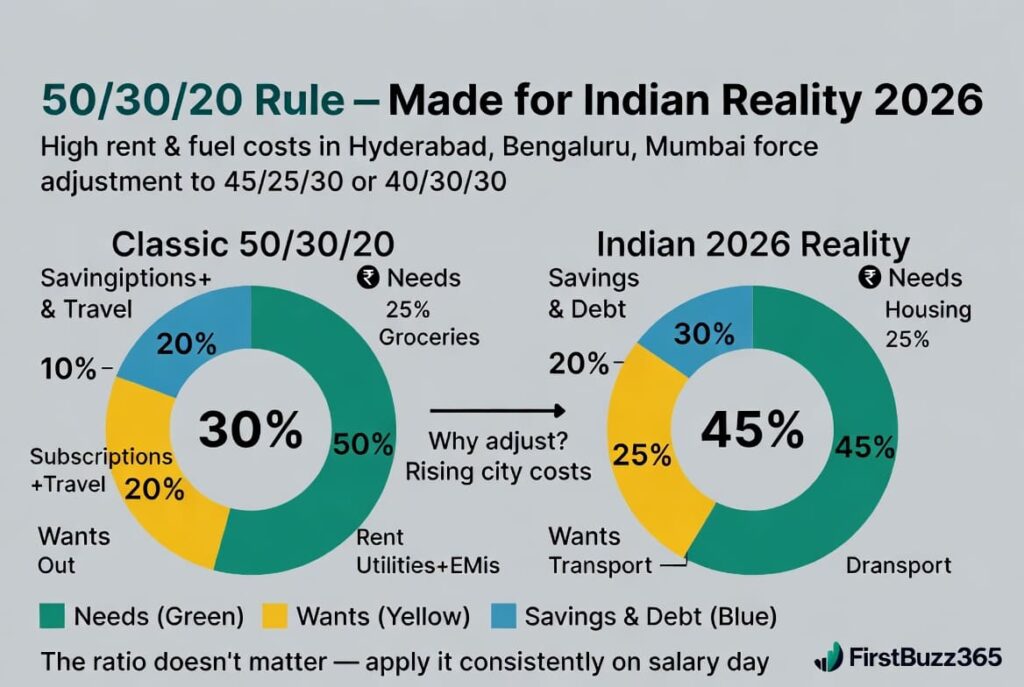

To start structuring finances properly, professionals suggest beginning with a realistic budgeting framework like the 50/30/20 rule: 50% on needs such as rent, groceries, utilities, and minimum EMIs; 30% on wants including dining out, subscriptions, and travel; and 20% on savings plus debt repayment.

In high-cost cities like Hyderabad, Bengaluru, or Mumbai, many adjust this to 45/25/30 or 40/30/30 to account for steeper housing and transport costs. The ratio itself isn’t as important as applying it consistently. Reviewing the last three months of bank and UPI statements to categorize every transaction often reveals ₹3,000–₹8,000 in monthly silent leaks from subscriptions, frequent food delivery, or impulse online purchases.

The Real Pain Points Most People Miss

Getting into what usually goes wrong helps avoid repeating common errors. One major issue is the mindset of “I’ll start managing money when I earn more.” This traps people because money habits scale with income. If ₹30,000 slips away easily now, ₹80,000 will vanish even faster later, just with better justifications.

Another common problem involves confusing lifestyle growth with financial growth. Buying better phones, cars, or vacations feels like progress, but true advancement comes from building financial buffers. Most prioritize upgrades in gadgets or trips while delaying emergency funds, insurance, or investments, leading to imbalance and later stress.

Overdependence on credit without full understanding ranks high too. Credit cards, BNPL apps, and instant loans seem convenient but turn dangerous when unmanaged. Credit serves as a tool, but used blindly, it creates traps that linger.

To counter these, adopt a quarterly review habit. Spend 45 minutes every three months checking one expense category to reduce by 15–25%, ensuring savings transfers stay automatic and consistent, and planning for upcoming large expenses like school fees, family functions, or device replacements. This simple routine prevents minor issues from snowballing.

Credit Score: The Number That Quietly Controls Your Life

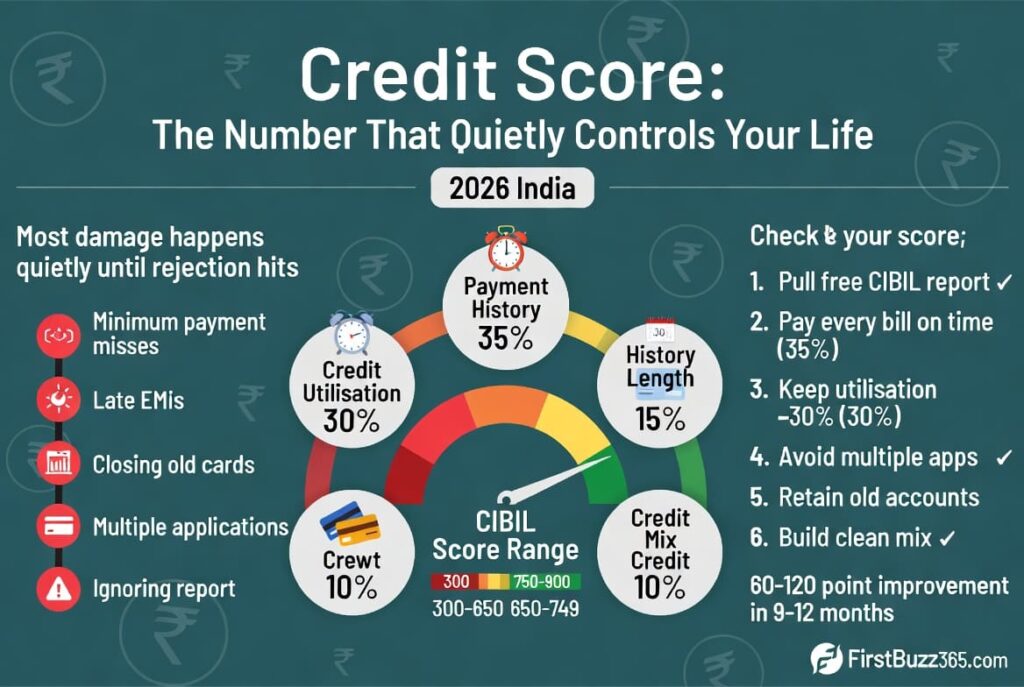

In 2026, credit scores matter more than ever for Indians. They influence loan approvals, interest rates, credit card limits, and even rentals or job background checks in some cases. A credit score is a number, typically between 300 and 900, that reflects how responsibly borrowed money gets handled. A higher score signals lower risk to lenders.

The score draws from several factors. Payment history checks if EMIs and credit card bills get paid on time. Credit utilisation examines if most of the limit is used, how long credit has been in use and evaluates handling of cards, loans, and EMIs properly. New credit behaviour flags too many loans or cards in a short time as a red flag. No need to memorize these—simply treat credit with respect, like a useful but unforgiving tool. New credit behaviour flags too many loans or cards in a short time as a red flag. No need to memorize these—simply treat credit with respect, like a useful but unforgiving tool.

Common mistakes include paying only the minimum due on credit cards, missing EMIs by “just a few days,” closing old credit cards unnecessarily, applying for multiple loans or cards at once, and ignoring credit reports until a loan rejection hits. Most damage happens quietly until it surfaces.

For credit score improvement in India, follow these basics in order: Pull the free annual CIBIL report and correct any errors immediately, pay every EMI and credit card bill on or before the due date (35% of score), keep credit card utilisation below 30% (30% of score), avoid multiple loan or credit card applications in short periods, retain older well-managed accounts (length of history matters), and build a clean mix of secured credit if no history exists. People who stick to this checklist often see 60–120 point improvements within 9–12 months.

The Basics of Saving (Before You Think About Investing)

Saving comes before spending, not with whatever remains. The first essential buffer is an emergency fund for medical issues, job loss, family emergencies, or unexpected repairs. It offers no returns or excitement—just safety. Without it, the entire financial structure stays unstable.

Single persons or young couples should aim for 6 months of expenses, families with dependents for 9 months, and self-employed or those with variable income for 9–12 months.

For a household with ₹65,000 monthly expenses, that means ₹3.9 lakh to ₹7.8 lakh in liquid, low-risk options like high-interest savings accounts, liquid mutual funds, or short-duration debt funds.

A helpful micro-habit involves rounding up daily UPI or card transactions—many accumulate ₹15,000–₹40,000 extra per year this way without feeling the pinch.

Tax Planning: Old vs New Regime (2026 Perspective)

Choosing the right tax regime saves money—don’t follow what others do. The old regime suits those claiming more than ₹3.75 lakh in deductions, including ₹1.5 lakh under 80C for PPF, ELSS, NSC, 5-year FD, or life insurance premiums; ₹25,000–50,000 under 80D for health insurance; home loan interest up to ₹2 lakh under Section 24; and an additional ₹50,000 in NPS under 80CCD(1B).

The new regime offers simpler slabs with no most deductions, making it better for those with minimal investments. Always simulate both options using trusted calculators like ClearTax, Groww, or the Income Tax portal before the financial year ends to decide objectively.

Investing Basics for Sustainable Growth

Investing starts only after establishing an emergency fund, insurance, and tax optimisation. For most Indians in 2026, sustainable growth comes from starting small and consistent with ₹2,000–₹5,000 monthly SIPs, preferring broad-market index funds or flexi-cap funds over individual stock picking for the first 5–7 years, allocating 50–70% to equity if under 40 and gradually reducing after 45, and rebalancing once a year rather than every month.

Historical data shows the Nifty 50 TRI delivering ~12–15% CAGR over rolling 10-year periods. Starting early and staying invested through volatility provides the most reliable path for middle-class wealth creation.

Retirement Planning – Updated 2026 Targets

Current estimates suggest a ₹4–4.5 crore corpus needed at age 60 to support a ₹60,000–₹80,000 monthly lifestyle, adjusted for 7% long-term inflation. Primary building blocks include EPF + VPF for 8.25% assured tax-free returns, NPS with active choice for up to 75% equity growth potential, equity mutual fund SIPs outside retirement wrappers, and health insurance continuation critical after 60.

An annual review checklist asks: Has the required corpus increased due to inflation or lifestyle change? Is the maximum possible being contributed to tax-advantaged vehicles? Is asset allocation still appropriate for age and risk profile?

Insurance: Protection, Not Profit

Insurance protects life, not grows money. Understand two basics: Health insurance, as medical costs rise faster than income, and term life insurance if someone depends on your income. If a product sounds too attractive as an investment, question it. Pure term life offers coverage of 15–20 times annual income, with ₹1 crore minimum for most earning members under 40. Health cover needs ₹15–25 lakh base family floater, with top-up or super-top-up for higher protection at lower cost. Avoid investment-cum-insurance products for wealth creation.

Financial Literacy in India: Statistics, Importance, and How to Start Structuring Finances in the Digital Era

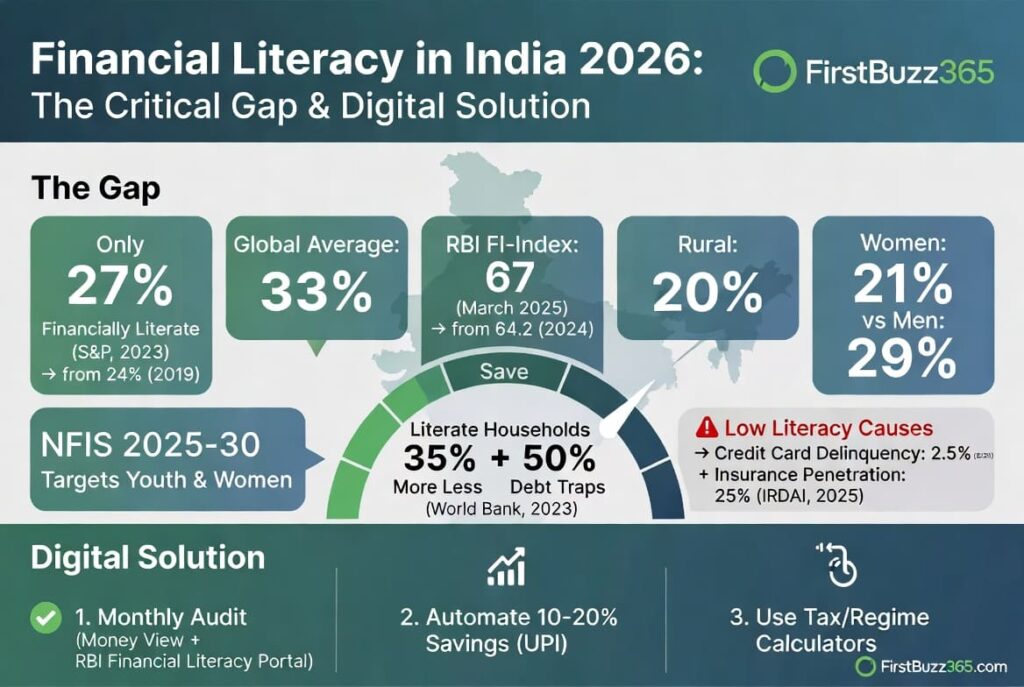

Financial literacy in India remains a critical gap, with only 27% of adults considered financially literate according to the 2023 S&P Global FinLit Survey (latest available as of 2026), up from 24% in 2019 but still low compared to global averages of 33%. The RBI’s Financial Inclusion Index (FI-Index) rose to 67 in March 2025 from 64.2 in 2024, driven by improvements in access, usage, and quality, which includes financial literacy elements (RBI release, July 2025). However, the National Centre for Financial Education (NCFE) 2023 survey showed rural literacy at just 20%, with women lagging at 21% versus 29% for men. The NFIS 2025–30 (RBI, December 2025) aims to boost this through targeted programs for youth and women.

Why is financial literacy important? It empowers individuals to make informed decisions, reducing poverty and promoting growth—literate households save 35% more and are 50% less likely to fall into debt traps (World Bank 2023). In India, low literacy contributes to high default rates (credit card delinquencies at 2.5% in 2025, TransUnion CIBIL) and underuse of tools like insurance (only 25% penetration, IRDAI 2025).

In this digital era, start structuring finances properly by leveraging apps for budgeting (e.g., Money View for tracking), online education platforms (Khan Academy or RBI’s financial literacy portals for free courses), and digital banking (UPI for seamless transfers, auto-SIPs via Groww). Begin with a monthly audit, automate 10–20% savings, and use calculators for tax/regime simulations—digital tools make it easier to stay consistent and informed.

Age-Wise Reality Check (Because Advice Is Not One-Size-Fits-All)

Students and early earners should learn budgeting early, avoid unnecessary credit, and build habits without pressure. Working professionals need to balance lifestyle and future, protect income with insurance, and build long-term investments. Business owners and freelancers face irregular income, so planning becomes critical, emergency funds matter more, and separating business and personal money is key. Different stages share the same principles.

The Most Important Personal Finance Skill (Rarely Taught)

It’s not investing, budgeting, or earning more—it’s decision discipline. This involves not upgrading everything at once, not following every trend, not comparing with others, and not panicking during setbacks. Money rewards patience more than intelligence.

Final Words: Control, Clarity, and Calm

People don’t need to master finance—just understand the basics, avoid obvious mistakes, and stay consistent longer than others. Personal finance isn’t about perfection; it’s about control, clarity, and calm, achievable at any income level.

What You’ll Find Next on FirstBuzz365 (Personal Finance Series): How credit scores are built and repaired, simple budgeting systems for Indian households, debt vs savings—what to prioritize, real-life financial mistakes and lessons.

FirstBuzz365 — The Buzz That Actually Helps.

What is the single biggest financial question on your mind right now? Leave a comment.

Download the a free “FirstBuzz365 Financial Clarity Sheet Pro tool” with embedded formulas to help readers gain financial clarity. Download it here to track expenses, calculate emergency funds, simulate tax regimes, and monitor credit utilisation—all in one simple Excel sheet tailored to give our readers gain clarity.

FirstBuzz365_Financial_Clarity_Sheet_Pro (0 downloads )