Personal Finance Basics India 2026: Budget, CIBIL, SIP, Tax

A real-money guide for people who learned this stuff the hard way — budgeting, CIBIL, SIPs, taxes, insurance, and the mistake nobody warns you about personal finance

By the FirstBuzz365 Editorial & Research Team | Updated: 2026 | ~15 min read

There was never a real conversation about money in my house. And honestly, there wasn’t one at school either. Twelve years of education — quadratic equations, the water cycle, the causes of World War I — and not a single class on personal finance, how a credit score works, what an EMI actually costs you over time, or why term insurance exists.

Nobody thought to put it in the syllabus. It just wasn’t considered a life skill worth teaching formally.

My father said ‘CIBIL’ the way some parents say ‘don’t run near traffic’ — urgent tone, zero explanation.

A warning without a lesson. What it meant, how it was calculated, what you were actually supposed to do to protect it — none of that ever followed.

The credit card I got at 24 — I understood the limit, not the interest. A family medical emergency in my mid-twenties made the gap between ‘having a salary’ and ‘having savings’ uncomfortably clear. And somewhere around 28, I sat down and did the math on three years of decent income and found almost nothing to show for it. No single catastrophe. Just slow, invisible drift.

India in 2026 is a genuinely complicated place to manage money. Rents in Bengaluru and Hyderabad are brutal for anyone in the first decade of their career.

while you’re navigating EMIs, family expectations, and an Instagram feed full of people who look financially sorted in ways that probably aren’t the complete picture.

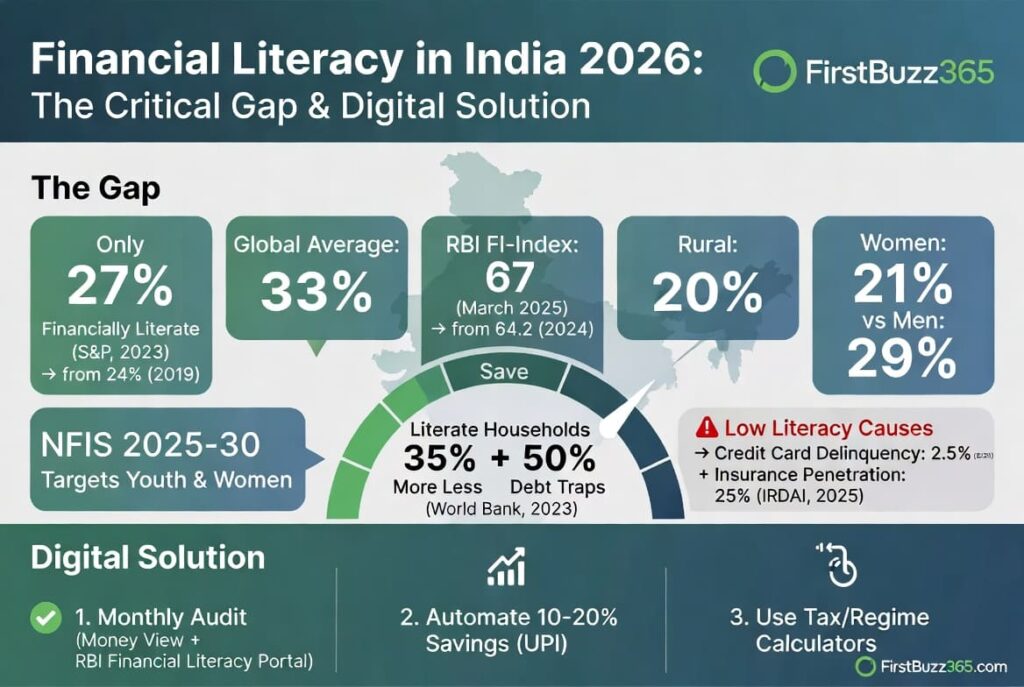

The NCFE estimates that only 27% of Indian adults are financially literate — a number that hasn’t moved much despite years of government effort. Globally, the average sits at 33%, and India still hasn’t reached it.

The RBI’s Financial Inclusion Index climbed to 67 in March 2025, up from 64.2 the year before DD News — driven mostly by UPI adoption and Jan Dhan reach rather than actual financial knowledge. 18% of women in India remain unaware of any financial inclusion scheme at all, and while 69% of women use digital banking, only 44% transact regularly EY.

The World Economic Forum found that 51% of Indian individuals struggle to meet their debts and liabilities — nearly double the global average of 32% World Economic Forum. Insurance penetration still sits below 5% of GDP per IRDAI data. These aren’t abstract statistics — they explain why the people around us keep making expensive, avoidable mistakes with money.

1. What Personal Finance Actually Is

Personal finance is every decision you make about money — how you earn, spend, save, borrow, multiply, and whether you’ve built any protection if things go sideways. That’s the whole thing.

The textbook version — ‘management of individual financial activities’ — is technically correct and completely useless in practice. In real life, personal finance is the conversation with your partner about whether to prepay the home loan or keep the SIP running. It’s the moment you scroll through last month’s UPI history and land on a Zomato total that surprises you. It’s the trip you decided not to book because you finally have three months of savings and you’re not ready to touch it.

The six pieces that make up the picture

Income — salary, freelance, side work, property rent. Expenses — fixed things like EMIs and rent, variable things like groceries and the impulse purchases you’ve stopped tracking. Debt — home loan, education loan, credit card balances, that personal loan from 2022 that you’ve half-forgotten. Savings — the buffer you’re building, starting with the emergency fund. Investments — what’s actually growing your money over years. And protection — health insurance and term life, the two things most people don’t think about until they desperately need them.

Getting these six into rough balance is the whole job. Not perfection. Just paying attention to all six, instead of only the one that’s currently making you anxious.

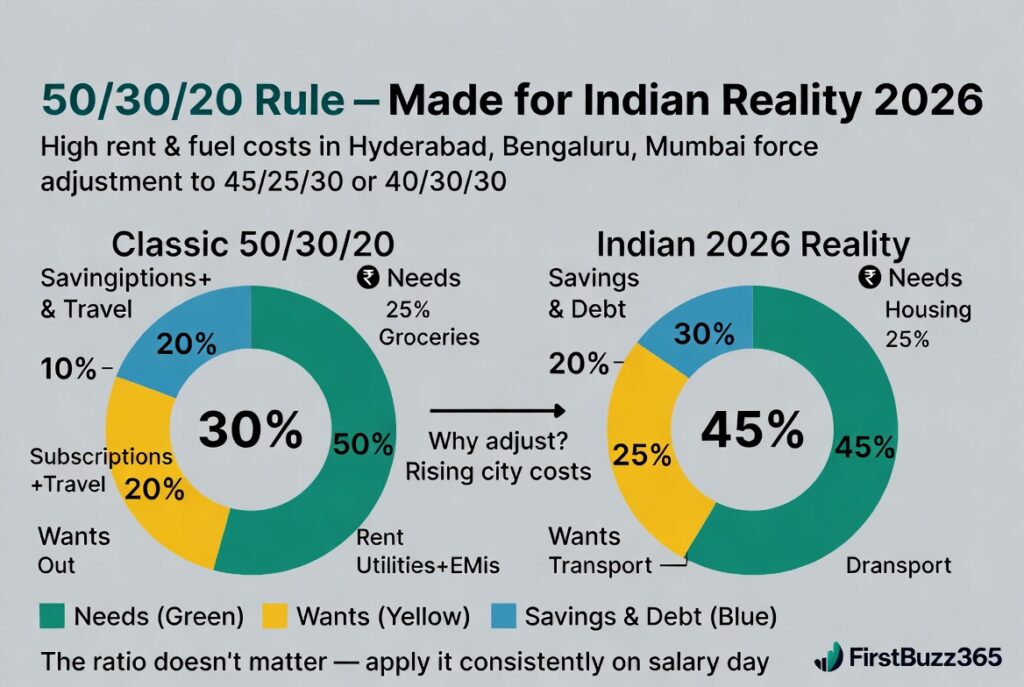

The 50/30/20 rule — and why it needs adjustment for India

Fifty percent of take-home pay goes to needs: rent, groceries, utilities, minimum EMI payments. Thirty percent to wants: dining out, streaming, the trip you keep postponing. Twenty percent to savings and debt repayment. That’s the rule. Reasonable starting point.

Except if you’re renting in Koramangala or Bandra, ‘50% for needs’ isn’t achievable — rent alone can eat 35–40% of a ₹50,000 take-home. So you adjust: 45/25/30, 40/30/30, whatever keeps savings from going to zero. The percentages matter less than building the habit of allocating deliberately at all.

Worth doing this week: download your last three months of UPI and bank statements and go through every line. Categorise it. Most people find ₹3,000–₹8,000 in monthly leaks they’d stopped noticing — old subscriptions still running, food delivery that felt small per order but added up, random purchases that seemed fine in isolation. The total is almost always higher than you’d expect.

2. The Patterns That Keep People Stuck

Enough conversations with people in their late 20s and 30s about money, and the same patterns keep surfacing. Three of them are consistent enough to be almost universal.

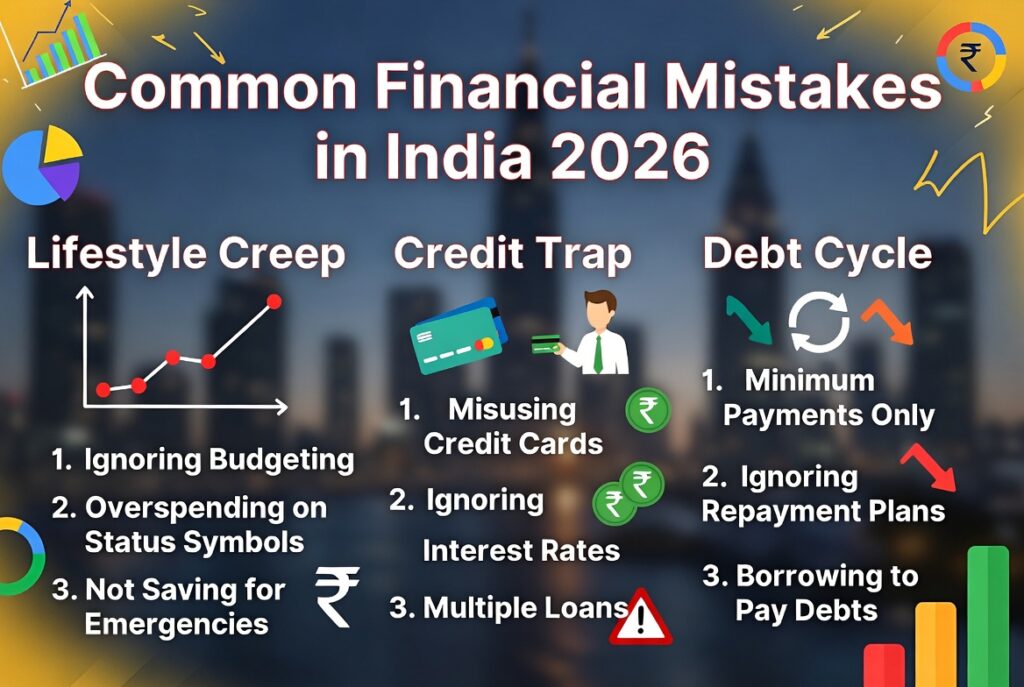

‘I’ll get serious about money once I earn more’

I said this for years. Sounds logical — more income, more to work with. The problem is it doesn’t hold. A friend went from ₹30,000 to ₹1,20,000 a month over six years. Savings rate barely moved. Every increment got absorbed quietly: a better apartment, more flights, upgraded gadgets, nicer restaurants. The excuses got better. The outcome stayed the same.

Habits scale with income. If there’s no structure at ₹30,000, it won’t appear on its own at ₹80,000. The structure has to come first, even when it feels premature.

Confusing lifestyle upgrades with financial progress

The new phone, the Goa trip, the car — these feel like your life improving. And they’re not necessarily wrong choices. But financial progress looks quieter. It looks like an emergency fund that didn’t exist a year ago. A term insurance policy that means a tragedy won’t also be a financial catastrophe. A SIP that’s been running for four years without being touched once.

In the early years, lifestyle progress and financial progress often run in opposite directions. That tension is real and it doesn’t resolve — you just learn to manage it consciously instead of by default.

Credit is easy to get and genuinely hard to understand

Buy Now, Pay Later (BNPL) apps, instant personal loans, credit cards with ₹1 lakh limits — in 2026 you can get substantial borrowed money in about ten minutes. The ease of access and the real cost of repayment are two very different things. I’ve seen people build up ₹2–3 lakh in credit card rollovers without fully registering it happened, because the minimum-due option always felt manageable in the moment. That’s exactly the problem.

What helps with all three: one 45-minute session per quarter — not monthly, that becomes a chore — where you look at where money actually went, confirm savings are landing where you think they are, and think ahead to anything expensive coming up. Catching a problem in April costs much less than catching it in June when it’s already a crisis.

3. Your CIBIL Score — What It Actually Affects in 2026

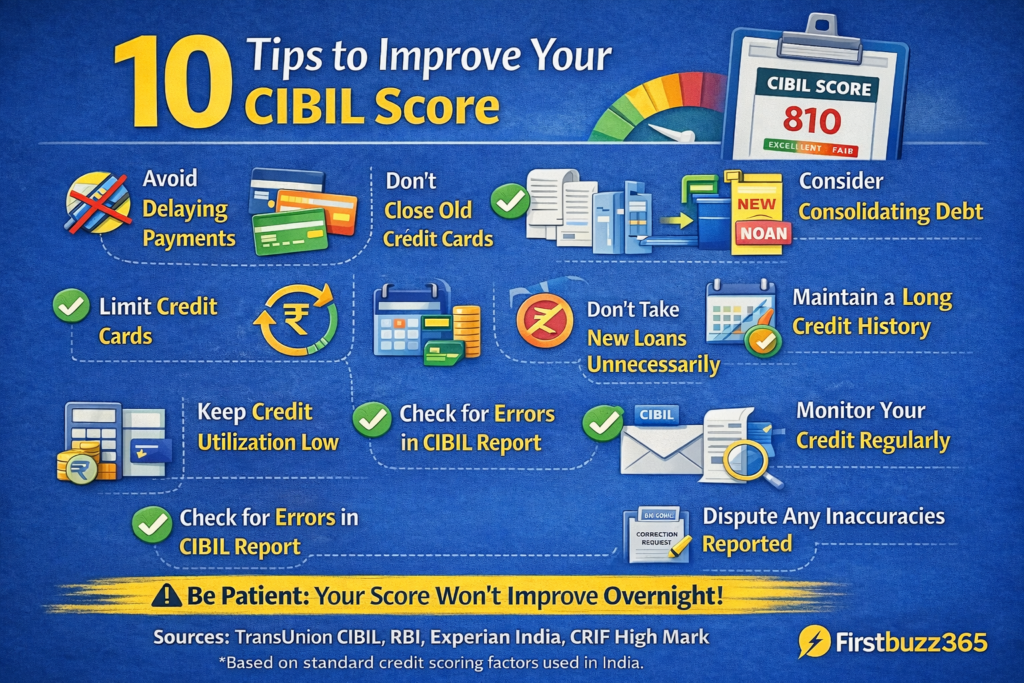

Your CIBIL score isn’t just about loan approval anymore. It affects the interest rate you’re offered — on a ₹50 lakh home loan, a 1–2% difference between a 750 and an 800+ score is a significant amount of money over 20 years. Some landlords now check it before agreeing to a rental. Some employers run it for background verification in finance roles. Range is 300–900. Anything above 750 opens most doors.

Five things determine the number: payment history, credit utilisation (what percentage of your available limit you’re actually using), length of credit history, mix of credit types, and recent applications. Payment history and utilisation together account for roughly 65% of the score — and both are completely within your control.

What quietly drags it down

- Paying only the minimum due every month. The interest on the remaining balance runs at 36–42% annualised on most cards. It compounds faster than most people realise.

- Being a few days late on EMIs. The grace period doesn’t work the way people assume on most products.

- Closing an old credit card you’ve held for six or seven years. Credit history length takes a hit and recovers slowly.

- Applying for three credit products in two months. Each hard inquiry shows up, and multiple in a short window signals risk to lenders.

- Never checking your CIBIL report. Errors are more common than people realise — wrong accounts, closed loans still showing active. You’re the only one who will catch them.

The checklist, in priority order

- Pull your free annual CIBIL report first. Dispute any errors before doing anything else.

- Pay everything on or before the due date, every single month. This alone fixes most score problems over time.

- Get utilisation below 30%. If your total credit limit is ₹1 lakh, keep balances under ₹30,000. Below 10% is better.

- Avoid applying for multiple credit products in a short window.

- Keep your oldest accounts open and lightly active.

- Building credit from scratch? A secured credit card — backed by a fixed deposit — is the cleanest starting point.

📋 Quick action: Pull your free CIBIL report at CIBIL’s official site — one free report per year, takes under five minutes. Most people are surprised by what they find.

Consistent effort on this checklist over 9–12 months typically produces 60–120 point improvements. There’s no shortcut faster than paying on time and keeping utilisation low. Anyone promising quicker results is selling something.

4. Building Savings — Foundation Before Everything Else

The order that matters: emergency fund before investments. Always. Before the SIP, before stocks, before topping up NPS. Emergency fund first.

‘Emergency fund’ sounds like advice you’ve filed away. Here’s what it actually looks like when it doesn’t exist. In 2021 I watched a family navigate a sudden hospitalisation. They liquidated a two-year-old SIP at a loss. Took a personal loan at 18% interest. Borrowed from two different relatives. All of this simultaneously while dealing with the actual emergency. An emergency fund doesn’t earn impressive returns. What it does is stop one bad month from undoing years of careful work.

How much you actually need

- Single person or couple without dependents: 6 months of monthly expenses

- Family with kids or aging parents depending on you: 9 months

- Freelancers, consultants, variable income: 9–12 months minimum

For a household spending ₹65,000 a month, that’s ₹3.9 lakh to ₹7.8 lakh kept liquid. Not in a 5-year FD. Not in equity. In a high-interest savings account, a liquid mutual fund, or a short-duration debt fund — something accessible in 24–48 hours without penalties.

One thing that genuinely works for building this fund: open a completely separate savings account just for it. Then mentally round up every transaction and let the difference accumulate there. People who do this consistently often find ₹15,000–₹40,000 extra at year end — without it ever feeling like deprivation. Money sitting in your main account gets spent.

5. Tax Planning: Old vs New Regime in 2026

Don’t just do what your colleague does. Don’t take your CA uncle’s advice without running your own numbers first. The right regime depends entirely on your specific deductions, and the difference can easily be ₹20,000–₹80,000 in a single year. It’s worth fifteen minutes.

Old regime works if your deductions cross ₹3.75 lakh

- Section 80C — up to ₹1.5 lakh: PPF, ELSS funds, NSC, 5-year FD, life insurance premiums

- Section 80D — ₹25,000 for self/family health insurance; ₹50,000 if covering senior citizen parents

- Section 24 — up to ₹2 lakh on home loan interest

- Section 80CCD(1B) — extra ₹50,000 for NPS contributions, over and above 80C. Most people miss this entirely.

New regime

Cleaner slabs, lower rates, almost no deductions. If you’re early in your career and haven’t built up 80C investments yet, this is probably better for you right now. Same if you’re renting rather than paying a home loan EMI — the deductions simply aren’t there to justify the old regime.

6. SIP for Beginners — How to Start Without Overthinking It

Right order: emergency fund first. Term and health insurance second. Tax planning sorted. Then investing. Going straight to stock picking without this foundation is like tiling the bathroom before laying the foundation slab.

For most people new to investing, SIP — Systematic Investment Plan — is the most practical entry point. You pick an amount, pick a fund, set up auto-debit on your salary date, and it runs without requiring your attention. No timing the market, or watching Sensex at 9:15 AM. No panic during corrections — or ideally no panic, which is the actual discipline.

How to actually get started

- ₹2,000–₹5,000 a month is a fine starting range. The amount matters far less than the habit of leaving it alone.

- First five to seven years: broad index funds or flexi-cap funds. Not individual stocks or sector bets.

- Under 40: 50–70% equity allocation makes sense for your time horizon.

- Rebalance once a year. Not when the market falls. Not when it rises. Once a year.

The Nifty 50 TRI has delivered roughly 12–15% CAGR over rolling 10-year periods historically. Nobody knows what the next decade brings. But time in the market has consistently beaten timing the market for most retail investors. The biggest mistake: starting a SIP, watching it dip 15% in a correction, and stopping. That’s precisely backwards — corrections are when units are cheapest.

The amount you start with matters less than starting. A ₹500 SIP at 22 ends up contributing more to your final corpus than a ₹5,000 SIP started at 35, purely because of how much runway compounding gets to work with. Ten years of doing nothing dramatic beats most clever strategies.

7. Retirement Planning — 2026 Numbers Worth Knowing

The number worth having in your head: ₹4–4.5 crore at age 60 to support a ₹60,000–₹80,000 monthly lifestyle, assuming 7% long-term inflation. That sounds enormous. It is a large number. It’s also genuinely reachable if you start consistently in your 30s with the right instruments — and it becomes very difficult if you keep moving the start date forward.

EPF and VPF

8.25% annualised, government-guaranteed, completely tax-free at maturity. If you’re salaried, EPF is already running. VPF — Voluntary Provident Fund — lets you contribute beyond the mandatory amount at the same guaranteed rate. It’s one of the best risk-free returns available in India and almost nobody uses it as aggressively as they should.

NPS (Active Choice)

National Pension System on active choice gives up to 75% equity allocation. Returns are market-linked and historically competitive. The extra ₹50,000 deduction under Section 80CCD(1B) — over and above the 80C limit — is free tax saving that most salaried employees leave unclaimed.

Equity mutual fund SIPs

Your primary wealth-building engine outside tax-advantaged instruments. This is where the bulk of long-term corpus should be built.

One thing people consistently overlook: health insurance as a retirement tool. Medical costs after 60 are one of the biggest threats to any retirement corpus. A hospitalisation that runs ₹8–10 lakh can erase a year of careful saving. Get adequate coverage before 60 — premiums are dramatically lower when you buy young.

8. Insurance — Get These Two Right and Stop Overthinking

Two products. That’s this entire section. Get these two right and the insurance chapter of your financial life is sorted.

Health insurance

India’s medical inflation runs well above general inflation. A moderate private hospital stay — three or four days, standard procedure — comfortably runs ₹3–5 lakh in metro cities. ICU or major surgery is a completely different number. Without insurance, one medical event can undo years of saving.

Every earning adult needs at minimum a ₹15–25 lakh family floater. Layer a super top-up plan on top — cheap, high coverage above a deductible — for broader protection at manageable additional cost.

Term life insurance

If anyone depends on your income — partner, parents, children — this isn’t optional. Pure term cover at 15–20x your annual income. For most working adults under 40, that means ₹1 crore minimum. Bought young, the premium is genuinely affordable. It gets expensive when you buy late and unavailable when something’s already wrong with your health.

Worth being direct about this: any product that claims to be both a great investment and solid insurance simultaneously is almost certainly mediocre at both. ULIPs and endowment plans consistently underperform pure mutual funds on returns and pure term insurance on protection. Keep the two completely separate. This one decision probably saves more money over a lifetime than almost any other single financial choice.

9. Financial Literacy in India — Where Things Actually Stand

The headline: 27% financially literate adults as of 2023. The details: credit card delinquency rates hit 2.5% in 2025 per TransUnion CIBIL. Insurance penetration just 25% per IRDAI 2025. Rural financial literacy at 20%. Women’s at 21%, men’s at 29%.

The National Financial Inclusion Strategy 2025–30 has targets for improving all of this. Government policy timelines are slow. Your own decisions move faster.

Tools worth using regularly

- Track spending with Money View, your bank’s app, or even a plain notes file. The specific tool matters far less than the habit.

- Learn for free: RBI’s financial literacy portal, NCFE resources, SEBI-registered advisor channels on YouTube. The quality of free content available now is genuinely good.

- Automate everything possible — UPI scheduled transfers, SIP auto-debits. Systems outlast willpower month after month.

- Simulate old vs new tax regime on ClearTax or the Income Tax portal before every financial year closes.

The simplest system that actually works: on salary day, move 10–20% to savings and SIPs before a single rupee goes anywhere else. Then spend what remains. This one structural change, consistently applied, does more than any other single financial habit.

10. Money Priorities by Life Stage

The fundamentals don’t change across life stages. What deserves the most attention does.

Students and early earners (20–26)

This is when the habits form — and when lifestyle inflation is most tempting, because you’re watching friends spend freely and benchmarking yourself constantly. The habits built here carry forward for decades. Track spending. Understand credit before using it. Don’t let every salary hike automatically become a lifestyle upgrade. A ₹500 SIP at 22 isn’t about the ₹500 — it’s about the compounding time you’re locking in.

Working professionals (27–40)

Compounding works hardest for you right now, which means delay is most expensive right now. Lock in insurance. Increase SIP amounts with every hike, even partially. Build the retirement foundation. Don’t let this decade slip by with ‘I’ll get serious about this soon’ — that sentence has cost people more than most bad investments.

Business owners and freelancers

Irregular income changes everything structurally. Emergency fund minimum goes to 12 months. Tax planning needs to be proactive — advance tax, quarterly estimates, not a scramble in March. Most important: keep personal and business finances in completely separate accounts. Mixing them is one of the most common, most damaging, and hardest-to-reverse mistakes in this group.

11. The One Skill Nobody Teaches

The skill is doing nothing dramatic when everything around you is screaming to do something dramatic.

Not selling when the market dropped 20% in 2024, or moving savings into whatever sector the office group chat was convinced about. Failing to upgrade everything the month the hike came in. Not measuring your actual financial situation against what you see on Instagram — which leaves out the EMIs and the anxiety and the gaps.

Most people who end up in genuinely solid financial shape at 55 or 60 didn’t do anything brilliant. They started early enough, stayed consistent, avoided catastrophic mistakes, and resisted the urge to blow up a working plan every time something new and exciting appeared. Patience is worth more than cleverness here. Most of the real damage to personal finances doesn’t come from not knowing enough — it comes from acting too much, too impulsively, too reactively.

12. Frequently Asked Questions

What is the 50/30/20 rule and does it work in India?

It divides take-home income into three buckets: 50% for needs (rent, groceries, utilities, EMIs), 30% for wants (dining out, travel, subscriptions), 20% for savings and debt repayment. In Mumbai or Bengaluru where rent alone takes 35–40% of income, adjusting to 40/30/30 is more realistic. The habit of allocating deliberately matters more than the exact split.

How do I improve my CIBIL score quickly?

There’s no genuine shortcut. What consistently works: pay every EMI and credit card bill on or before the due date, keep utilisation below 30%, and check your CIBIL report for errors once a year. Sustained effort on these three things typically produces 60–120 point gains over 9–12 months.

What is SIP and how do I start as a complete beginner?

SIP — Systematic Investment Plan — is a monthly auto-debit into a mutual fund of your choice. Beginners can start with ₹500–₹2,000 in a broad-market index fund or flexi-cap fund. Set up auto-debit on salary day and don’t touch it when the market dips.

How much emergency fund do I need in India?

6 months of monthly expenses for individuals or couples without dependents. 9 months for families with children or aging parents. 9–12 months for freelancers or anyone with variable income. Keep it in a liquid mutual fund or high-interest savings account — not a long-term FD.

Old or new income tax regime — which is better in 2026?

Depends entirely on your deductions. Old regime wins if you claim over ₹3.75 lakh (80C + 80D + home loan interest + NPS). New regime is better for early-career earners with minimal deductions or anyone renting rather than servicing a home loan.

How much do I need to retire comfortably in India?

Current 2026 estimate: ₹4–4.5 crore at age 60 to sustain ₹60,000–₹80,000 monthly, accounting for 7% long-term inflation. Built through EPF, NPS, and equity SIPs started in your 30s, this is achievable for most salaried households. Every year of delay makes the number harder to reach.

What’s the simplest way to manage money on a salaried income?

On salary day: automate 10–20% to savings and SIPs first. Maintain an emergency fund. Max out 80C. Hold term and health insurance. Run a SIP even at ₹500. Review once a quarter. Consistency beats cleverness every time.

How do I save money in India on a tight income?

Start with a UPI statement review — find where money is actually going. Cut recurring leaks first: subscriptions, daily food delivery. Automate ₹200–₹500 to a separate account on salary day before spending anything else. The structural habit of saving first and spending from what remains works at every income level.

Final Thought: Clarity

You don’t need to be an expert. You need to be consistently decent — decent saving habits, decent investment discipline, enough awareness to know what your money is actually doing. That’s genuinely enough to end up in a much better place than most people around you.

Whether it’s fixing your CIBIL score, starting your first SIP, figuring out how to actually save on a salary that doesn’t stretch as far as you’d like, or just reaching a point where you’re not lying awake anxious about money — every step compounds. The same way the money does, if you give it time.

The FirstBuzz365 Financial Health Dashboard (free download below) puts everything from this guide into one Excel sheet: expense tracking, emergency fund calculator, tax regime simulator, credit utilisation monitor.

→ Download the Free FirstBuzz365_Financial_Health_Dashboard_PRO_2026 [link]

The FirstBuzz365 Financial Health Dashboard PRO 2026 is a free Excel workbook that puts your entire financial picture in one place — built specifically for Indian earners navigating salaries, EMIs, taxes, and long-term goals in 2026. It doesn’t just show you numbers. It tells you what those numbers mean and what to do about them.

How to use it — 5 minutes to get started

- Open the file and go to Sheet 2 — Income & Profile. Fill in your monthly income, age, and employment type. Everything else calculates from here. Sample data is pre-filled for a ₹60K Bengaluru professional — just replace it with your numbers.

- Enter your debts (Sheet 3) and monthly budget (Sheet 4). List your loans and EMIs. Fill in what you budget vs what you actually spend. The dashboard immediately shows your EMI load, savings rate, and monthly surplus — colour-coded green, yellow, or red.

- Check the Leak Finder (Sheet 5) and set your Goals (Sheet 7). Enter discretionary spending to see the real cost. Then add up to 10 financial goals — the sheet tells you exactly how much to save monthly for each one.

- Run the Tax Regime Selector (Sheet 10) before March. Enter your salary and deductions once. The dashboard compares both regimes with full 2026-27 calculations and tells you which one saves more — and by exactly how much per month.

- Check your Health Score and Master Dashboard anytime. These two sheets update automatically from everything you’ve entered. No extra work — just open them after any update to see your current financial position and what to prioritise.

- Readers walk away with a clear view of their actual monthly surplus or deficit, the right tax regime for their situation with exact monthly savings, and the precise SIP needed to reach their target retirement income. They also get a prioritised list of three actions based on their own data, visibility into hidden spending leaks with their long-term compounded cost, and a financial health score they can track and improve over time—not just a one-time audit.

Disclaimer

FirstBuzz365 — The Buzz That Actually Helps.

What’s the single biggest financial question on your mind right now? Drop it in the comments.